34 min read

Media Sector Trends and Challenges

Read time: 60 mins

Introduction

This article expands on our in-depth read Introducing the Version 1 Media Sector Impact Dial. Here’s another look at the dial.

The global media market is predicted to grow to over $2.9tn by 2026 from around $1.9tn in 2017, a near 50% growth in just under a decade. Other research predicts a 4-5% onward compound annual growth rate. So, there is ample opportunity for media organisations to grow, adapt and embrace the macro forces impacting the sector. The dial covers a large number of topics and each is covered in turn to explore the major trends we have identified as most impactful to media and publishing today.

- Introduction

- Globalisation & Market Expansion

- Sector Disruptions and the Creator Economy

- Demographics and E-Commerce

- Conclusion

- Version 1’s Media Sector Expertise

- Blog Sources

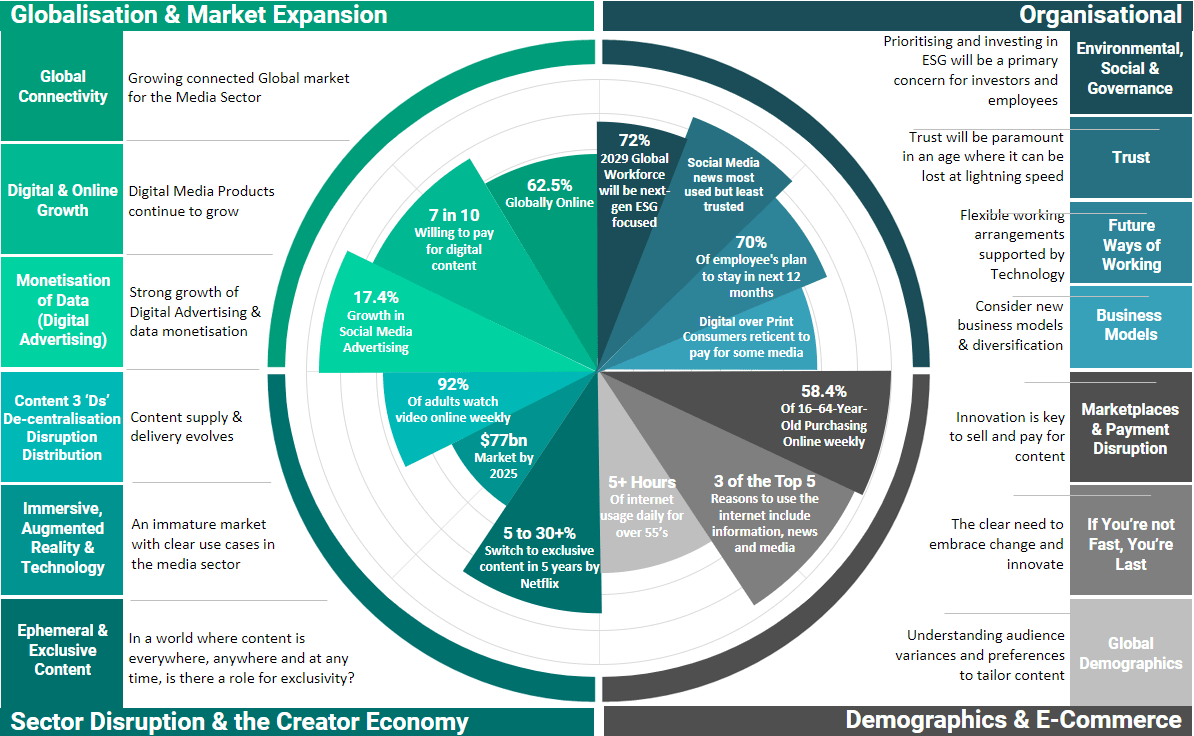

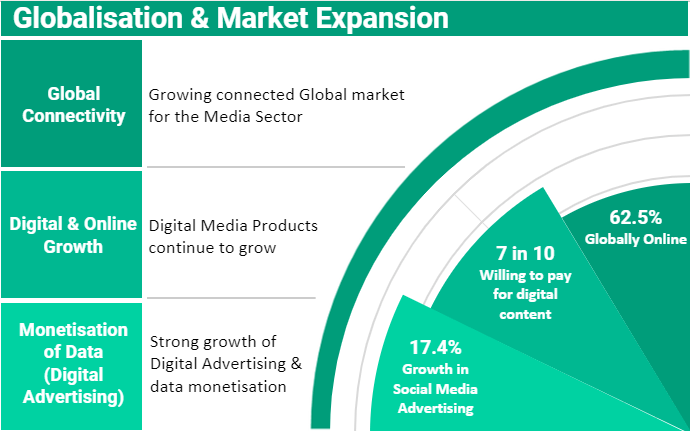

Globalisation & Market Expansion

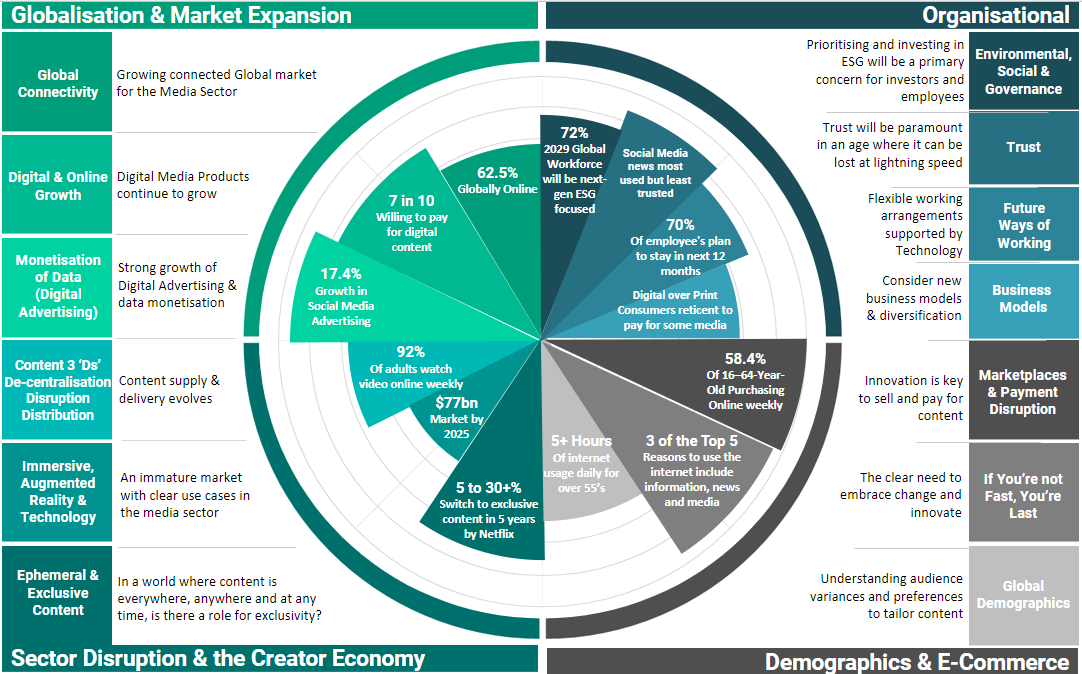

Not all media organisations are global, but it is certain that global trends will impact how the sector grows and evolves. The digital world has no boundaries, and for the media sector this is especially true. We are going to look at the global market in three key groupings and how they might impact the sector. The groupings are global connectivity, digital and online growth and the monetisation of data (Digital Advertising).

Global Connectivity

It is estimated that there are now 4.95bn internet users, over 62% of the global population. Regionally, areas such as in the southern hemisphere (e.g., Ghana, Nigeria, Kenya) have larger proportions that remain offline compared to the global average. Europe’s offline population is still around 78 million, indicating that there is still room for audience growth all over the world.

Trends show that we will soon hit 5bn internet users and as more and more regions establish robust infrastructure to allow more of the population to go online, it is likely, it is likely to provide increasing opportunities for the sector to diversify. More subscribers, more producers and consumers, and more markets with which to target compelling digital content.

Global growth is the backdrop to this evolution and the effects of global events are also hugely important. Regional instability such as the war in Ukraine or the ongoing impacts of the cost of living crisis’ are just a couple of examples that can and do introduce negative impacts. For example, the recent rises in costs of energy have impacted traditional print publishers who have seen their costs rise. We’ve also seen big names such as Netflix and Disney lose subscribers, perhaps due to economic factors and changes post-lockdown. Netflix and others have withdrawn from Russia due to the Ukraine war, losing some 700,000 subscribers. These examples and many more are why global factors are such an important part of how the sector develops, receiving both strong tail winds and the occasional need to ‘batten down the hatches’ when an economic storm comes along. We’ll discuss some of these tailwinds throughout this blog.

Digital and Online Growth

‘Digital is king’. You only need to look at some of the big tech players to see the continued growth of digital content. YouTube’s global advertising audience has surpassed 2bn, up almost 12% in the past year. Instagram’s advertising audience is almost 1.5bn, up 21% on the previous year. TikTok has reached 885m users (aged 18+), with 7% growth in a quarter and estimates almost half of all US adults use TikTok every month (despite attempted bans).

GWI research also reveals that 7 in 10 working internet users (16-64) are now willing to pay for digital content with Video and Media being some of the top choices. And of the total spend on Digital media globally ($293.9bn), almost $86bn was for video on demand and a further $27.6bn on e-Publishing.

GWI also state that the average social media user spends 2.5 hours on social media per day (the equivalent of 4 trillion hours a year). Social Media usage grew just over 10% in 2022 to just over 4.6bn users globally.

PWC estimate 4% annual growth for the Media Sector within the UK through to 2026, driven primarily by digital adoption and digital offerings across multiple channels. But its important to note that its not always a ‘rosy picture’. As I mentioned previously, post pandemic, some of the big global streaming platforms have had to cope with decline in subscriptions, despite the allure of exclusive content. Showing that when the purse strings are tight, streaming subscriptions may be the first cut in any household budget’

And considering the previous points about online growth, it is also estimated 31.9% of the global population are using language translation weekly. Technology such as GTP3/4 (Generative Pre-Trained Transformer 3) uses deep-learning to produce human-like text, providing the opportunity for consumers to easily translate your written content.

Brand also remains a key factor in digital and online growth with mergers and acquisitions (M&A) remaining a fact of life for media outlets. It is likely that such M&As will be increasingly based on transactions that allow the expanded organisation to innovate, build brand and reach new markets. This will be influenced by a drive to differentiate from competitors and retain subscribers and readership. Digital content and delivering over new and innovative channels will be a key aspect across the board. And the drive for new digital content over new channels coupled with future regulation will mean publishers having to place privacy and cyber–security at the top of their agendas to protect not only their brand and IP, but also to provide confidence to their readership in an increasingly digital world.

All media organisations must focus on digital content and offerings to remain relevant. Not only will it out-strip print, but it also opens new revenue streams such as digital advertising and access to new markets globally.

Monetisation of Data and Digital Advertising

For media, data-driven advertising remains a key area of growth and is backed up by global trends such as the growth of Social Media advertising which is up 17.4% in 2022 to $154bn – approximately one third of all digital advertising. Tailoring advertising based on data, information, and insights determinable across multiple channels is a key method of data monetisation.

The power of this can also be seen by increasing costs; the average cost per 1,000 paid social media advert impressions is up almost 22% in a year at $9.13.

Most recently we see giants such as Netflix and Disney introducing cheaper, ad supported tiers. It’s part of a strategy to address losses in subscribers – Netflix lost 200k in Q1 2022, a chunk of which were long term users. Disney+ lost 2.4m subscribers in Q3 2022. Whilst the strategy is attempting to counter cancellations, it also opens up alternative revenue streams. As both hold information about their subscribers, content viewing history and content preferences, they are well placed to provide valuable data to digital advertisers.

Data is therefore increasingly being monetised and valued as an asset. For example, captured form data and curated content can be repurposed into a new revenue stream. Monetising this information is a fundamental element to drive advertisement revenue, particularly when played out over multiple and innovative channels.

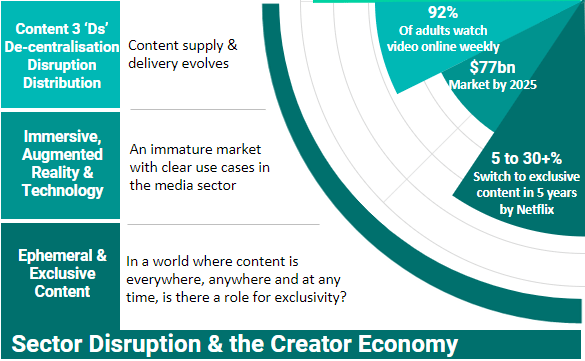

Sector Disruptions and the Creator Economy

Modern technologies, innovation and digital transformation has seen the rise of ‘big-tech’ (YouTube, TikTok, Instagram, Facebook, Twitch, Spotify etc.) which deliver popular services to the individual. That same individual can now create and distribute their own content with ease, generate income and become online social influencers, even entrepreneurs. And as we live in a 24×7 news cycle, with the public as first-hand witnesses to breaking events, the same individuals can record, upload and stream video through social platforms in near real-time. This significantly shortens the breaking news cycle and presents an opportunity to leverage public, creator and influencer content for more engaging customer experiences and revenue. For the younger demographic the rise of the influencer also provides an ability to engage directly with the audience.

The 3 ‘Ds’ of Content

We believe content is being affected in three main ways:

1. It’s no longer centralised and under the sole control of the media industry such as the news channel or newspaper publisher.

2. It has also been and continues to be disrupted from both ends – by the big names such as Netflix and Amazon along with the individual, ‘the citizen journalist’, the influencers and freelancers.

3. Finally, it has moved away from coming via a few channels such as state broadcasters or a national broadsheet, rather many (increasingly digital) channels carry content.

Content de-centralisation is not only about who authors and distributes content but the many channels that carry it. For example, 92.1% of internet users (4.95bn) now have access to mobile devices, so they can consume information anywhere at any time. Now, citizen journalism allows these users to be content creators as eyewitnesses to events, international, national, or local.

When it comes to distribution, we can see examples in the older demographic, (55–64-year-olds). It is estimated they spend 5 hours 13 minutes daily online, giving easy access to engage with this age group which previously may have relied more on print. Connected TV is the fastest growing form of internet medium at 10.5% growth per annum reaching 30.4% of current internet users. Smart Home devices are also growing, reaching 13.8% of online users, 17% year on year growth.

Disruption can take many forms. For example, influencer videos are estimated to account for nearly 27% of watched video content each week with nearly 92% of those 16 to 64 watching some form of video weekly. Across Europe the social media user base as percentage of population is generally above 70% and as high as 85% in Northern Europe. Also, reading news stories for Social Media users is higher at 31.6% than other reasons such as watching sport, other live streams, and even product purchases.

This multi-lens disruption – from big platforms, from social media and from citizen journalism is a challenge. The media sector must compete and maintain brand trust as well as embrace the diverse ways content is created and consumed. As a small example, some publishers do embrace the market; The New York times offers $1,000 for personal essays, the Chicago Tribune offering $150 to $500 for travel articles. In the UK, many newspapers’ offer money for news stories which can be submitted online. Embrace the ‘3D’s’ of content, don’t avoid them.

Immersive, Augmented Reality, and Technology

The immersive technology sector is expanding globally. In 2020 5.5 million virtual and augmented reality headsets were shipped, expected to rise to 43.5 million by 2025. The growth rate is expected to be around 22.3% a year, reaching $18.6 billion by 2026. The virtual world market value is estimated to reach $77 billion by 2025 with the biggest commercial use cases being training, industrial maintenance, and retail (itself a key source of advertising). Citibank forecasts that the metaverse represents an opportunity of between $8-13tn through to 2023.

However, all may not be what it appears. The market is not yet mature, nor is the opportunity clear for the media sector. Big-tech has seen significant restructuring of late but notably Meta, the owners of Facebook, have sought to reduce their global workforce by around 13% in light of poor quarterly results. Forbes, in a recent article described the investment in the metaverse by Meta as “a solution in search of dozens of problems” and while “we cannot predict where tech will take us in 10, 20 or 50 years…. the metaverse…..day is not now, it’s not tomorrow and it may not get here before Meta runs out of money or its investors run out of patience”.

Yet, clear use cases exist. Companies such as IKEA, Audi and Airbus have adopted a VR experience with strong results. For the media sector, the most interesting use cases centre on gaming (61%), education (41%), movies/TV (21%) and marketing/advertising (16%). Sports media has introduced AR experiences in their publications, allowing an athlete to leap out of the page to take part in an interview on your phone. This can revolutionise the way in which media is consumed by connecting the public with celebrities, in their own virtual world. One interesting example was a golf tournament in South Korea which was broadcast with a metaverse layer, adding new experiences for viewers.

A virtual world waiting to be explored? Interestingly, Gartner predicts 25% of people will spend at least 1 hour per day in the metaverse by 2026. PWC see the adoption of VR and AR by younger demographic as the next generation of digital advertising, entertainment, and brand experience. They cite brands such as Nike and Gucci as not only offering virtual items for purchase but also offering the opportunity to order the physical equivalent. Within media, the opportunity is to tap into the realism and immersive experience – when Google first provided street view, viewers of maps could suddenly zoom in and see the area being explored. Might the broadcast of news for example follow a similar pattern the viewer can explore a virtual story in tandem with the news report?

Time of course, will tell. The jury is out on how this technology will unfold, but it’s not going away (Apple only recently announced their $3,500 Vision Pro, an advanced AR headset in a world where AR has never really arrived). The younger generation, who are purchasing headsets and accessing immersive content in a virtual world may well be the drivers for change in the long term – and in setting the pace of adoption for media organisations.

Public Cloud. In terms of other technology, we predict a growing trend toward cloud adoption, cloud-first, or cloud-only strategies within the media sector. Our recent migration experience with an international publisher and broadcaster who looked to a cloud-first strategy to reduce operational costs and time to market of content and services has seen them consider a large-scale multi-datacentre, multi-location migration to the cloud. This was for an organisation with multiple brands and titles, looking to drive efficiencies and consolidation through cloud adoption.

Cloud helps to drive increased automation through infrastructure as code and deployment, whilst leveraging consistent and repeatable results. We have also seen many of our media sector customers look to highly automated next-generation managed services which offer high or hyper-automated in the cloud to generate maximum operating efficiencies whilst increasing quality and innovation in the service.

Technical Debt Constraints. We also know that current legacy technology and technical debt is a constraint for most major publishers – and may be common across the sector. These hinder agility and growth, so it is an important consideration for publishers to evolve to new technologies that not only address technical debt, but create efficiencies in operation, reduce costs and ultimately deliver tangible business value such as audience growth or increased revenue. Public cloud helps to address some of these legacy challenges.

Sentiment Analysis is another key technology in the media sector. We have developed our own sentiment analysis solutions for some of our customers such as the Criminal Cases Review Commission (CCRW) where our SmartText solution used AI, sentiment analysis, topic modelling and semantic search to analyse electronic documents to extract and group relevant information much faster than a human could. In the publishing space for example, the use case for such technology is obvious, with an increasing level of written and un-structured digital content being provided.

Data driven is always forefront. We have discussed previously the need to monetise data through data driven analytics. Taking publishers as an example, driving up Advertising revenue by using data is all about readership and subscriber behaviours to provide a customised and targeted experience – and effective advertising. It will also assist with determining which content is working and which isn’t.

Embracing big-tech. The sector also needs to embrace the global big-tech and social media platforms as well as building their own channels. Many businesses have grown by leveraging big-tech e.g., Netflix, built on AWS cloud, decided during the COVID pandemic to launch an Instagram live series, allowing their audience to connect live with mental health experts. Harvard Business Review offered free access to resources, promoted over social media, driving traffic from their social accounts to their website.

And let’s not forget AI! It would be hard to escape the buzz around AI in recent months and the breakthrough of generative AI (such as ChatGPT, Bard and MidJourney). The use cases in the media sector are varied, some well understood and others still gestating. In our blog introducing our sector impact dial, we listed some of the clear use cases from identifying ‘fake news’, to plagiarism identification, sentiment analysis and subtitle generation. We’d highly recommend any media organisation consider how they use AI and look to the innovation it might bring. Big names in the sector are already doing this – the BBC has a Research & Development project looking at how AI can assist in media production by freeing up producers and editors to focus on more creative and value-add tasks. For example, they are looking at AI to enhance the editing process by reducing the labour of assembling the best footage and freeing up time for the editors to make creative decisions. Google recently had their own blog on AI in the media sector and see it with three lenses:

- Improving content creation, production, and management.

- Enhancing and personalizing audience experiences.

- Improving monetisation.

Generative AI in the media sector could be used to curate content, flag offensive material or automate production elements. Automated journalism is an interesting area for Generative AI, with clear benefits in freeing up resources and outlets like MSN, The Associated Press, CNET and BuzzFeed have experimented with it.

There are warnings here too; bias, hallucinations, data privacy security are but some of the factors to be considered when using AI. Our recommendation would be to look at practical use cases, experiment and innovate whilst being fully aware of these potential issues. Media CIO’s who do not work to include AI are likely to be surprised down the line on the implications it has had on the sector.

Overall, our message is to look at the broad spectrum of technology trends and incorporate them into a forward-looking technology adoption roadmap such as outlined in our separate sector and technology radar blog.

Ephemeral and Exclusive Content

In the modern world, almost everything you might want is available online, anytime. This open market is the driver of the internet, social media, digital advertising, and brands. However, such inclusivity can be argued to de-value content or products that are perhaps of higher value or seen to be exclusive.

It is estimated that brands spend up to 43% of their marketing budget on content, yet only 23% of CMOs feel they are producing the right content for the right audience, at the right time and in the right format.

Exclusivity drives revenue. As an example, the fashion brand Balenciaga in 2021 wiped all its social media accounts ahead of revealing their haute couture collection. The strategy made customers work harder to find out about the products, which allowed Balenciaga to highly targeted content direct to the customer via social channels.

And you only need to look at the reason many subscribers sign up to Netflix, Amazon Prime Video or Disney+. In 2021 a survey of U.S. subscribers signing up to Netflix determined that 88% did so to access exclusive content, 59% stating it was the primary reason. And Netflix raised their spending on exclusives to $6.2bn that year. Netflix’s original content accounted for 12% of the most popular titles available across streaming platforms in the U.S. in Q1 2022. By March 2022, over 30% of their content was original, compared to 5% in 2016. Netflix, despite subscriber retention challenges and slowing growth, remain fairly bullish about streaming and exclusive content in general.

But what is the impact? These examples show the power of exclusive and ephemeral content for a business – it can drive revenue and raise brand awareness. This also challenges more traditional competitors such as national broadcasters whose license fee model and public charters may struggle to compete. Surveys prior to the pandemic suggested that platforms such as Netflix and Amazon Prime Video were seen as largely ‘additive’ to national broadcasters with traditional TV penetration up as much as 15%. We can see similar in the sports broadcast rights, where the exclusivity of the sport is the source of attraction for the content provider. In 2021 the BBC received many complaints about the lack of live Tokyo Olympics coverage, with viewers unaware the rights were held by Discovery.

Intellectual Property Rights (IPR) and Tracking. This topic also leads into IPR and tracking for many media organisations such as publishers. Protecting your digital assets, company brand, logo and unique content is as important as ever. But in a digital age that brings other challenges from the ease of distribution globally of online content, to the lack of any physical reproduction barriers, the ease of production copying and distribution of digital content, the difficulty in the ability to enforce rights online and that IP law globally is not a universal interpretation. The Organisation for Economic Co-operation and Development (OECD) and the EU’s Intellectual Property Office claim that trade in counterfeit and pirated goods stood at 3.3% of global trade, whilst in the U.S., the FBI’s IPR unit estimated the cost of counterfeit goods to the U.S. economy stood around $600bn annually. There is hope however, and media organisations need to look to technology to help protect and enforce IPR on their digital content. The use of technology-based solutions such as AI, that we already touched on, can help. Big tech has already developed solutions such as Apple’s Digital Rights Management for music. In the e-commerce world, big-tech platforms also provide solutions such as Amazon’s Brand Registry Tool (users reporting 99% fewer infringements) and Facebook’s Rights Manager. There is no easy answer or silver bullet, and media organisations will need to take a holistic approach to their IPR rights on digital content from their own network protections to digital rights management.

As we move forward the media sector is likely to see greater emphasis on exclusive and limited time content. Depending on your organisation, this may have positive or negative consequences. Certainly, as discussed for traditional broadcasters, it is likely to place pressure on existing license fee models and their ability to compete commercially. For publishers, this may be more around brand exclusivity, the trust in or reputation of the name and therefore the content provided. Most media organisations need to look to exclusive and ephemeral content to generate revenue and retain consumers.

Demographics and E- Commerce

We have already discussed aspects of the demographics of the global online generation; but it is important to understand this huge topic in a little more detail, even if that is only to ‘scrape the surface’ – and indeed how these demographics affect the wider digital economy that surrounds them.

Global Online Demographics

As we mentioned, the world is on course for 5bn online users – most of the world’s population will have internet access. But usage of online services, products and content vary across age groups and from region to region.

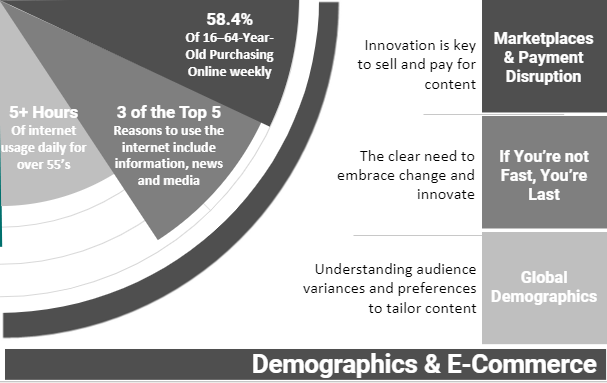

A Tech-savvy and tech-hungry growing market. Looking at social media, ages up to 59 account for most social user accounts, tailing off to just 4.4% of females and 4% of males over 60. The young (16-24’s) are more likely to use online translation tools over older adults, hinting perhaps at a more globally connected next generation. This same trend continues for other technology areas such as image recognition and voice assistant technology. The next generation are increasingly becoming tech savvy and looking for new ways to engage in the digital age. However, even for older adults, it is estimated that over 55’s spend as much as 5 hours per day using the internet, rising to 8 hours for the 16–24-year-olds.

Younger audiences tend to prefer video over reading, particularly on social media. 31.8% of 16-64 years old pay for video streaming, a further 17.9% for video downloads and 53% of children in the UK own a smart phone by the age of 7. And if we consider how the younger generation might access content over a range of platforms, it makes the current rise in cost of print likely to be a long-term challenge as the future of printed material tries to compete.

This has wide ranging and deep impact. Such changes in behaviour requires the sector to plan for the future and to respond with the relevant content and delivery channels. However, that is not just about streaming your latest video, it must be supported by an end-to-end process. That process would include the entire content supply chain through to consumption and archival. Taking journalism as an example it will span identification of the lead, the journalism or filming involved, content authoring, editorial processes, content distribution, how that content was received and consumer response to it as part of a continuous improvement loop.

Another interesting aspect of these changing demographics is the link with brand. Younger viewers, and indeed some older ones, may be more interested in streaming certain shows or content e.g., World Cup, Bake Off, I’m a Celebrity Get me Out of Here and Love Island. They have a connection not with the content creator or provider but the content itself. Providers are keen to provide other ways to engage this audience, through social media and other platforms. I’m a Celebrity has its own Twitter feed, Facebook page, is linked with the presenters own social media accounts, is on streaming and broadcast and even has its own spin-off shows. And all provide different ways to engage the viewer, advertise and generate revenue.

In the newspaper publishing world, the impacts have already been seen. Newspaper expenditure fell from £4.45bn in 2005 to £2.8bn in 2020, a fall of 37%, whilst newspaper circulation has been declining for several years. Despite this though, the share of consumers over 16 in the UK reading news online has increased by 50% between 2007 and 2020.

Media organisations need to keep pace with their audience and respond to the changing behaviours of consumers. Traditional methods might still have a role, but it would be wise to supplement these with new digital content and channels.

If You’re Not Fast, You’re Last

As we discussed in the creator economy, the modern world is a place where anyone can make and share content or breaking news at any time. Look at the recent British tourist who scribbled on the walls of the Coliseum in Rome, recorded by a passer-by who informed the authorities and shared it to social media. The tourist faced a fine of up to €15,000 and/or a prison sentence, as well as a public apology. All a consequence of his action which went viral online.

Data and content are increasingly real-time and ubiquitous, in contrast to the gated legacy content owned by most media companies. Most online audiences are looking for information, news, or video so it is essential that these companies plan for a future which delivers at least some of that constant stream of data.

Media organisations who do not innovate and adapt, may struggle. AI and Machine Learning can help to interpret video streams, extracting key information and metadata for onward processing. For example, AI can be used to monitor and extract insight from social media and other forums. Generative and Conversational AI, Natural Language Processing etc. can play roles in the interpretation of audio and text. They can also aid in analysing audience or consumer behaviours to drive more effective content and advertising. For those media organisations with access to historic content, digitisation of content mixed with AI can automate and accelerate its time to market, providing high-value insight and categorisations.

So as the saying goes if you’re not first, you’re last – getting your content out there, speed to market and tapping into your archive by making it more accessible are all key ingredients to growth.

Marketplaces and Payment Disruption

It is estimated that 58.4% of 16–64-year-olds purchase a product or service online weekly. These change over time, with online grocery shopping accounts for 28.3% of purchases each week currently. The purchasing options also have changed with 24.6% using an online price comparison service each week and 17.8% seeking a buy now, pay later service. Even across the age ranges, there is a reasonably steady rate of e-commerce at over 50% in each demographic. Notably digital media spend totals $293.9bn with video at $85.76bn and ePublishing at $27.59bn.

It is estimated 3.92 billion payments were made digitally with a 10% year on year increase in the number of people making digital payments from 2021 and with an estimated average of $1,766 per user.

Cryptocurrencies have arrived but mainstream adoption is slow. Bitcoin’s popularity surged in 2020 and 2021 with around 400,000 transactions a day in January 2021. Recent stats suggest Bitcoin has risen 67%, Nasdaq growth was a quarter of that number. These statistics suggest that crypto is here to stay, particularly in Europe, Africa, and Latin America. All this despite high-profile failures such as the bankruptcy of FTX and the arrest of its former CEO Sam Bankman-Fried in addition to scaling concerns for high transaction volume. The current economic gloom will certainly test the resolve of crypto.

These changes come as we have mentioned with a decrease in spend on print e.g., newspaper circulation, or pressure on public broadcaster license fee models, creating a ‘double whammy’ for some media outlets. As the marketplace moves on – and as consumers look to digital content and new ways to pay, the risk is media organisations could lose valuable revenue by not looking to their payment models and methods.

Organisational

This category deals with the impacts of change on the sector at an organisational level and some of the associated macro trends including:

- The need to consider new business models and diversification

- Future Ways of Working

- The need to establish and maintain Trust in your brand in the age when it can swiftly be undermined or lost

- The growing importance of Environmental, Social and Governance on the media organisation

Business Models

As discussed earlier, online payments and marketplaces will be a key driver for organisational business models into the future. The changing behaviours of consumers is also a big factor, as availability and performance of the internet moves consumption online – away from analogue, TV, paper books, newspapers towards online forms, mobile platforms and smart connected homes.

There are other challenges, research in the News industry suggests that while consumers prioritise digital publications over print, most consumers are reticent to pay for online news content. This has driven consumers to ‘free to use’ sources, helping to drive the popularity of social media and broadcast for news.

These changes are going to force media organisations to re-consider their business models and how they generate growth and revenue. We discussed how e-Publishing accounted for $27.59bn and video $85.76bn in spend, but these are also growing markets, the former growing at 12% and the latter at 21% year on year. These growing markets may present opportunities for media to curate content and deliver more personalised experiences to their consumers as is the case with advertising. Diversification of content may also be a factor e.g., online learning (57% of social media users state they would prefer to learn from social media video, via self-service content than via university content. And 14.4% of digital content purchases are e-learning, only 2.3% behind mobile games.)

Again, time to embrace big-tech. Organisations in the sector may need to consider embracing big-tech platforms as part of their operating model, looking to deliver content via social and other platforms as well as their own traditional channels. Like the examples in broadcasting, where TV shows will expand their reach to social media to engage their audience. Media organisations may also need to look to how they fund innovation by addressing debt operational expenditure to fund transformational investment whilst looking at how they can address efficiencies within their operating model.

The challenges in publishing. For publishing, the commercial and operational aspects of existing business models cover a wide range of trends and challenges. This ranges from accelerating publishing times to employee engagement and competition for skills. One example worth exploring is the rising cost of print. In the past, publishers tended to stay with the same printing provider as costs were relatively stable and fixed. However, in the past few years, print costs have risen due to inflation, rising paper prices, shortages in raw materials, Brexit factors, pandemic disruption of the supply chain and a significant rise in energy costs. All this means that across the whole sector, publishers are feeling the pinch. These factors in themselves over time are likely to be an accelerator for digital transformation and adoption. An example could be immersive virtual reality experience to engage a younger audience.

Broadcasters are also not immune! For national broadcasters, some of which Version 1 has worked with, there are various pressures on revenue streams (which largely have come from a license fee). These broadcasters are now facing tough competition and having to look at how they support content streaming in particular. They may also need to consider how they facilitate and re-purpose content to be delivered via an ever-changing set of channels e.g., PC, tablet, mobile, set-top box, YouTube etc.. They face real competition from internet only based content or niche rights-based digital content such as sports broadcast rights, where we have seen our customers face new competition through the recent COVID pandemic as sports adopted a pay-per-view model. In simple terms some organisations may need to consider the need to kill off legacy organs or risk dying alongside.

The simple truth is media organisations are going to have to develop business models that adapt, to consider forms of content previously not their mainstream business or use cases that diversify their portfolio whilst building the brand. Technology will play a part with consideration needed to SaaS or API driven revenue and monetisation of content.

Future Ways of Working

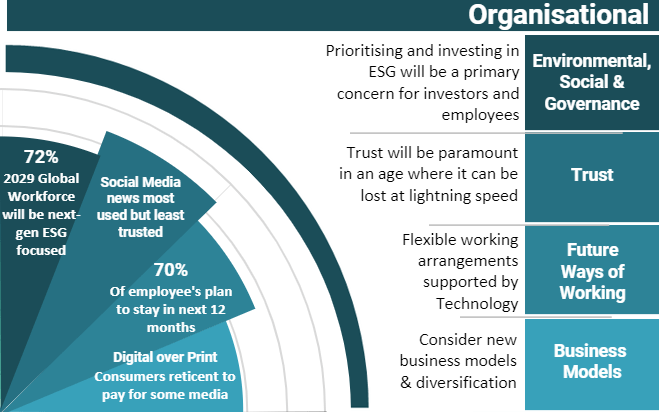

The Global Pandemic has had a lasting impact on ways of working and recruitment. The ONS Labour Force Survey in the UK indicates an increase in homeworking following the pandemic from 5% to 19% but as highlighted by the CIPD, other forms of flexible working have not followed suit with the number of workers in flexible arrangements such as job-share or flexible hours falling or remaining stagnant. And research suggests that workers at all levels want to adopt more flexible arrangements with 62% of senior executives and 58% of entry-level workers wishing to alternate between home and office according to the BCO.

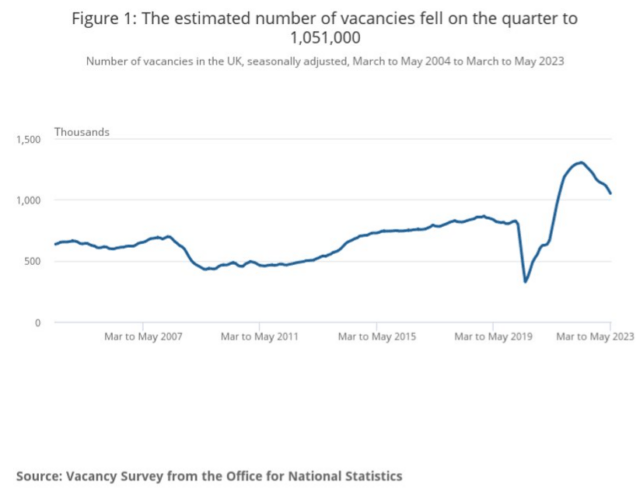

Workforce challenges. UK Government information also suggests over 1.2 million job vacancies at the end of 2021 – an all-time high (see ONS chart below). Post pandemic, more than half of businesses were unable to meet their recruitment demand and whilst this has perhaps eased e.g., in areas of the technology sector (with several big firm names having significant layoffs, placing individuals on the open market) trends still show a general challenge in recruitment. Interestingly a recent Recruitment and Employment Confederation (REC) report suggests that staff supply has expanded at its quickest rate since December 2020, cited by recruiters as being linked to economic uncertainty and redundancies but also workers being more willing to look for new roles for higher salaries.

Higher attrition rates and a competitive market also mean that once you secure the employee, retaining them is a key element of keeping a healthy workforce. 70% of employees stated they plan to be with their current employer in 12 months in 2022 according to MetLife, a marked downward trend from 80% in 2018, pre-pandemic. Employees also have clear driving reasons to stay with an employer including pay (39%), job security (38%), health benefits (34%) and finally flexible working at 29%.

The Global Pandemic has had a lasting impact on ways of working and recruitment. The ONS Labour Force Survey in the UK indicates an increase in homeworking following the pandemic from 5% to 19% but as highlighted by the CIPD, other forms of flexible working have not followed suit with the number of workers in flexible arrangements such as job-share or flexible hours falling or remaining stagnant. And research suggests that workers at all levels want to adopt more flexible arrangements with 62% of senior executives and 58% of entry-level workers wishing to alternate between home and office according to the BCO.

Content creator challenges. Content is no longer exclusively generated by the media – there is the creator economy and independent creators to consider in future ways of working. They have access to global platforms and large audiences. Media organisations will need to consider how these creators can be part of their own content process and supply chain, perhaps working collaboratively and openly with this group. Existing teams e.g., editorial teams may need to be re-structured to consider how content is re-purposed and edited from multiple sources and across geographies – and to leverage scale in their organisations.

The changing working landscape post-pandemic is not just for the media sector. However, like other sectors media organisations will need to find ways to address these challenges and adopt more open and flexible working arrangements for employees and the process of content creation, whilst offering a package that focuses on retention. Technology will continue to play an important part in this through remote and mobile working.

Trust

For mainstream media organisations, key to their reputation and growth will be the trust in the brand. They will need to focus on providing facts over personal opinions, politically charged content over neutrality and the continual challenge of ‘fake news’. Trust in content is also a key aspect, for example, the estimated doubling of deep-fake video every 6 months with only 7% deemed to have been created for comedy and entertainment purposes (cybernews.com).

Ensuring factual and impartial content. As we have discussed, the rise of the influencers and citizen journalism also presents trust challenges as these individuals are more likely to be emotionally biased and invested in the content they create. Social Media news for example, is the most used source of obtaining news but it also the least trusted by those who use it. If these sources are also used by your organisation there will be a requirement to effectively validate the content through the editorial process, even if the event is unfolding fast and in real-time. Consider the rise of Storyful, founded by journalists as the first social media newswire, utilising social content to add to news reporting.

In an online age when reputation can be made or lost overnight, it will be necessary for media organisations to maintain and protect trust in their brand. They must develop strategies to manage misleading information such as fact promotion over emotion, individual countermeasures, and active regulation of content. One only has to look at the challenges faced in platforms such as Facebook and Twitter on how, some argue, their platforms are used to disseminate misinformation or online harm. Digital IP ownership and digital rights are likely to play a part in marking and owning source content, whilst technology such as AI, BIAS and Analysis of Social Media feeds may be used to identify fake and mis-leading information. Media organisations may also have to look to their content supply chain to remove manipulation or influence. And in a world where 33.8% of users flag concerns on the misuse of personal data, losing your audience due to trust can have severe and lasting consequences.

Environment, Social and Governance (ESG)

“Looking at sustainability from the lens of the consumer”

ESG is becoming an increasingly important topic across all organisations, not just the media. Investment has doubled from 2016 and expected to surpass $50 trillion by 2025. One report states that as of 2020 88% of publicly traded companies, 79% of venture and private equity-backed companies and 67% of privately owned companies had ESG initiatives in place. Furthermore, 80% of the world’s largest companies are reporting exposure to physical or market risk associated with the current climate crisis. Governments are increasingly placing regulatory obligations on companies to have an ESG strategy and fund.

A consumer led lens. Knowing that a product, content or company is eco-friendly is stated as a factor for 20.6% of 16-64 years olds buying online (GWI Q3 2021 findings). The World Economic Forum places this much higher at 66% of all respondents and 75% of millennials saying they consider sustainability when making a purchase.

A workforce lens. Marsh McLennan report that by 2029, the millennial and Gen Z generations will make up 72% of the world’s workforce and will care more about environmental and social concerns and expect their employers to follow suit. Employee satisfaction is higher for those taking positive action on sustainability, mirroring the employees’ own values and give the work they do extra environmental meaning. Marsh McLennan say this also follows for organisations who have strong ESG scores over peer organisations.

Is digital always greener? Looking at newspaper publishing in particular, the decline of print is seen to have a positive environmental impact. However, digital content requires energy, lots of it. If you consider every step of the process of digital content, from its creation, to processing, transmission and viewing, all have a carbon footprint. Netflix estimates one hour of streaming by one user produces under 100g of carbon dioxide equivalent (CO2e), whilst the Carbon Trust states the European average is 55/56g of CO2e for every hour. Netflix also says users watched 6 billion hours of their top 10 shows in the first month of release. Using the Carbon Trust average that’s almost 1.13 billion miles of car travel. Whilst some may argue these emissions are still low in comparison to other activities, these industries will need to address the environmental impact in the future. In our view, the use of technology is still a massive benefit, but there is a responsibility to ensure that these activities are optimised for the environment.

Legislative and regulatory change is another risk factor for the sector in the UK as the Government, post Brexit, addresses the equivalent of the EU DMA (Digital Markets Act) alongside the Online Safety Bill – and introduces regulation such as the Age-Appropriate Design Code. The EU DMA, which came into force on 1st November 2022 aims to make the digital economy fairer and more competitive. Whilst these laws and regulations are aimed at some of the multi-national ‘Big-Tech’ platform providers such as Facebook, Netflix and Amazon, regulatory obligations often enshrine the protection of these platforms’ users. The concept will extend to digital content provided by publishers and advertisers to users, so content providers should also take heed. As an example, future digital content may make use of AI or sentiment analysis to detect compliance in real time rather than waiting for audience reporting.

The use of AI may come under regulation e.g., the AI Act is a proposal of the European Union as the first major law on AI anywhere, where three risk categories will be defined. The first is AI that creates unacceptable risk such as government-run social scoring, which will be illegal. The second involves cases such as CV-scanning to rank applicants which will be subject to specific legal requirements. Thirdly is others, where no regulatory requirements will exist. Version 1 is also a founding partner of the AI Assurance Club, along with a range of other organisations such as the Alan Turing Institute, EY and BSI. The aim is to provide a UK/EU wide forum for AI and ML ethics, regulatory compliance (UK and EU) and best practice.

The Media sector faces similar environmental, social and governance challenges as many other sectors and it will not be immune to the impacts of these as we have discussed. Media organisations will need to consider multiple aspects of ESG including for example:

- Digital inequality / Digital Divide by enabling access to content for all

- The use of modern technology to improve accessibility

- Committing to decarbonizing and putting the focus on the environmental impact

- The impacts of a changing regulatory and compliance landscape

Conclusion

So, we’ve taken a journey around our sector impact dial covering a very broad range of topics. We’ve shown that the media sector is facing many challenges. These are driven by the macro factors of globalisation, the place of digital content, the source of content, the expectations / behaviours of consumers and the pressures on media organisations to adapt. To help you prepare for these trends, we’ve also provided a simple positioning mechanism to do so, via media sector tech radar blog.

What does all this mean for your organisation and what have we learned?

There is an ever-growing global market for digital content. This market is a source of expanding and new revenue for media organisations, particularly in the field of digital advertising. In short digital content is king. Media organisations should be focused on a digital content strategy based on consumer behaviours and needs, ready to harvest data to deliver compelling content for users and advertisers.

There are ongoing challenges in the areas of authoring and distribution of content, the type of content produced, and the continued influence of new and innovative technology. Media organisations should embrace disruption. This means embracing new creators, enriching your supply chain, looking at other channels and researching new tech trends like VR to expand as needed.

Change is inevitable. Technology has changed how we create, view and pay for content. Traditional media organisations may face challenges of maintaining legacy elements of their business and need to consider new ways to engage consumers, adapt with the times, and deliver new ways for consumers to view and own content.

Organisational impacts are wide and deep. Media organisations need to examine the broad impact on their operations to keep pace with change. This includes new business models, addressing technical debt and new ways of working for employees. Brand trust will need to be protected and ESG will be of huge importance to employees and consumers. A developing and changing regulatory and compliance landscape will also need to be considered. This is a vast array of organisation change and media organisations would be wise to consider specific task forces to develop strategies in each area affected.

Data, data, data. Finally, to be effective, media organisations need to base content and decisions on data, harvesting and using it it to attract employees, consumers and advertisers. Media organisation should consider key data and analytics platforms to assists in the collection and collation of this data, the science behind the data and its effective us in the creation and distribution of content.

Version 1’s Media Sector Expertise

We come with an understanding of the media sector across the UK and Ireland. This includes well-known broadcasters, publishers, and content providers. We are a trusted partner to operate, innovate, and transform services across established players, including:

- International Published and Radio Broadcaster

- UK and Irish Newspapers

- European Telecommunications, and,

- National Broadcasters such as

Our collective experience tells us that things are moving quickly across the sector, but that the fundamental priority is still developing and distributing engaging, and increasingly digital content to drive audience growth and data-driven advertising.

Blog Sources

The following sources of research and information were used for this paper.