12 min read

Introducing the Version 1 Media Sector Impact Dial

Read time: 22 mins

Introduction – Opportunity & Growth in the Global Media Market

The global media market is predicted to grow to just above $2.9tn by 2026 from around $1.9tn in 2017, almost 50% growth in under a decade. Other research predicts a 4-5% onward compound annual growth rate and this is in the wake of a global pandemic, geo-political events, and a decade of content creation disruption from big-tech, not to mention the breakthrough of Generative Artificial Intelligence (AI).

As a global market, there is ample opportunity for those in the sector to grow by leveraging technology and consumer behaviours to deliver compelling, high-value content, and increasingly make use of what they know about the consumer to retain subscriptions or target advertising – protecting, growing, and opening new revenue in the process. However, to do so media organisations will need to embrace new ideas from content authoring to delivery – and beyond. Most of us are aware of the disruption the sector has faced in recent years, the rise of online streaming, social media platforms and changing consumer behaviours. This is set to continue with compelling macro forces likely to influence the sector over the next few years.

The sector is of course diverse and global media platforms may not be facing the same challenges as a UK publisher or national broadcaster for example. However, we want to provide an overall framework for the diverse nature of the sector to aid in summarising and classifying how these macro trends impact micro challenges – to do this, we are introducing our Sector Impact Dial.

- Introduction – Opportunity and Growth in the Global Media Market

- The Version 1 Sector Impact Dial©

- How to Read the Dial

- Globalisation and Market Expansion

- Sector Disruption and The Creator Economy

- Demographics and E-Commerce

- Organisational Influences

- Conclusion

- Version 1’s Media Sector Experiences

- Further Reading

- Blog Sources

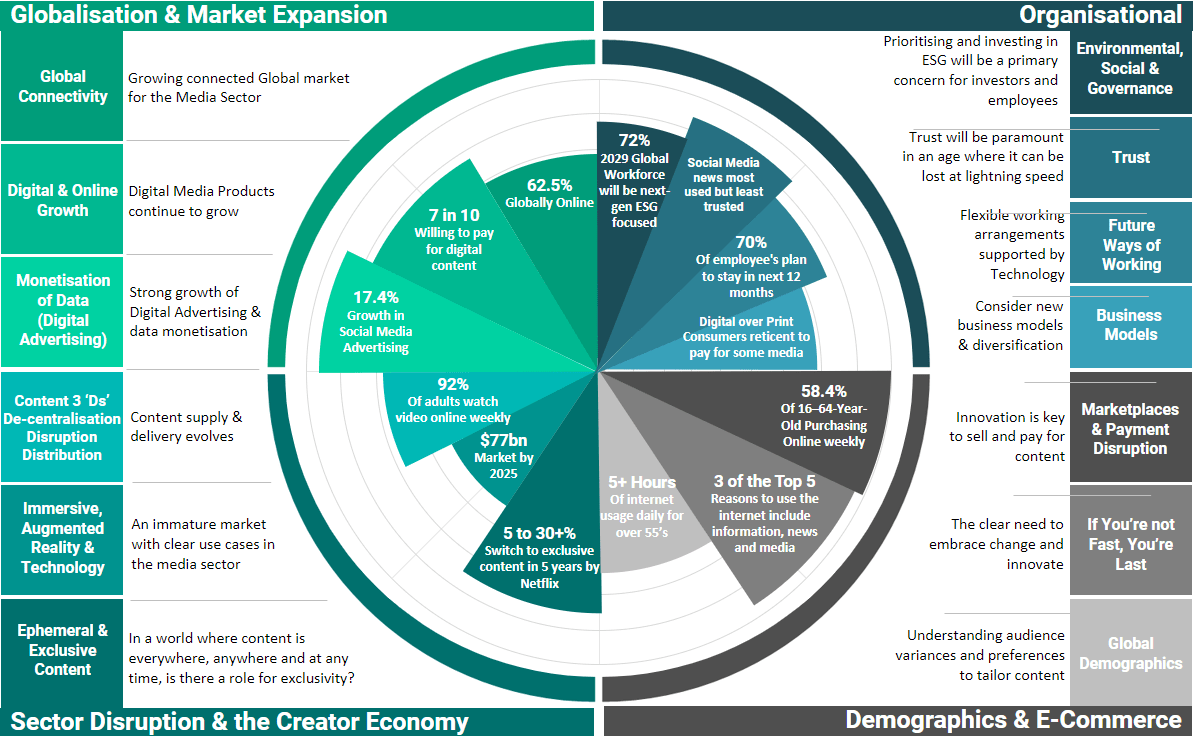

The Version 1 Sector Impact Dial

Version 1 has developed the Version 1 Sector Impact Dial. It is a guide to key trends and challenges, how to deal with them and rise to the challenge of embracing an increasingly digital world. The information presented here and in our associated in-depth read (Media Sector Trends) comes from public research, market statistics and our own insights and experience.

The Impact Dial is logically grouped into 4 key areas:

- The global market and global influences.

- Sector disruption including the growing content creator economy and emerging technologies.

- Organisational influences including the environment, trust and changing working patterns.

- The impact of shifting demographics and commerce.

Each area covers various sub-categories as shown in Figure 1 below.

How to Read the Dial

We discuss the various areas of the dial in greater detail in our separate in-depth read – Media Sector Trends and Challenges 2023.

Whilst all the trends shown above have an impact, the dial attempts to show our view of the relative impact of these trends in high-level terms. Your own organisation may be impacted differently depending on your specific circumstances.

A synopsis of our Media Sector Trends and Challenges 2023 is provided below.

Globalisation and Market Expansion

Whilst not all organisations operate on a global scale, global trends and forces have an impact on us all in some form and usually over time. For example:

- The global online internet user base continues to grow, with current estimates placing the global internet user population at just under 5bn. This of course masks some regional trends and less connected pockets but online audiences are growing worldwide. Most of us will have heard the joke about the essentials in life including Wi-Fi, but the reality is more and more of the world’s population is coming online and for media organisations that directly impacts content.

- Digital content is already driving growth. The success of the big tech firms from YouTube to TikTok and Netflix only show how they become global household names. They in turn are driving their own revenues via digital content and advertising. GWI research indicated that 7 in 10 are now willing to pay for digital content. In an increasingly connected world, providing compelling and engaging digital content is a necessary foundation for growth in the sector.

- And in this growing market, it is necessary to consider how your content and knowledge of your customers can be monetised to create a strong organisation. For example, Social Media Advertising is up 17.4% in 2022 to $154bn globally, indicating that many content producers are successfully leveraging their customer base to drive revenue. Sounds good, but in middle of all of this, the same organisations need to be flexible and adapt. We’ve seen the recent changes in approach by the likes of Netflix and Disney introducing cheaper subscriptions with advertising support, allowing both firms to drive and protect revenue. At the same time, post-pandemic, subscriber numbers have fallen, and we see the same organisations increase fees or clamping down on password sharing. Those in the sector needs to adapt or die and do so quickly.

Sector Disruption and the Creator Economy

Media companies are no longer the sole custodians of content. Today, almost anyone can publish their own content to a large audience in real time, 24/7. In a breaking news scenario, media outlets may find it harder to command the narrative as they did before. Content creation is being disrupted, de-centralised and increasingly distributed by the public at large.

The rise of the younger generation of influencers also sees new consumption patterns. Influencer videos are now estimated to account for 27% of watched video content each week.

Technology has and continues to disrupt the sector with the results yet to be fully understood. The ‘virtual world’ market is estimated by some to reach $77bn by 2025. Apple announced their augmented headset the Vision Pro, and newsfeeds are filled with stories about AI and Generative AI, including the likes of ChatGPT, Bard and MidJourney.

The commercial uses for immersive technology, perhaps outside of gaming and some commercially successful applications (e.g., Ikea, Audi and Airbus), are yet to be fully proven but media as a sector cannot ignore it – or do so at their peril. It’s likely that this future virtual and augmented world will be the domain of the younger and up-coming demographic, and what seems like a stretch today may be tomorrow’s mainstream distribution channel. Just look at this recent example of bringing a concert to life via Augmented Reality.

Immersive technology isn’t the only game in town of course, there’s also AI which can be used in the media sector in lots of interesting ways, including:

- Identifying ‘fake news’

- Rooting out plagiarism

- Sentiment analysis and personalised content

- Social Media platforms are already using AI – look at Facebooks use of facial recognition for example.

- Content creation including what some term ‘automated journalism’.

- AI generated images, video and music

- Subtitle generation

- Content targeting

- And more

AI is a whole topic on its own right, we have dedicated AI Labs here at Version 1 and several customer initiatives are already underway. AI also comes with some health warnings, from ethical and legal concerns to concerns about bias, and data security questions. Whilst we recognise all of this, any media sector CIO would be wise to begin to consider the use cases of AI, and recent developments within their own organisations. Like many organisations outside the sector, a strategy should be in place to research, innovate and utilise AI, whilst educating the organisation and customers in the process.

The final area of sector disruption comes in the form of exclusive and ephemeral content. In a world where just about everything is available online and consumers expect it to be a few clicks away, the need to protect digital content is only growing. The success of brands such as Netflix, Amazon, and Disney+ has been driven by exclusive content – some 88% of U.S. subscribers stated that they signed up in part because of this. And this exclusivity can drive revenue, particularly if coupled with a time-bound availability. One example is the fashion brand Balenciaga which wiped all its social media accounts ahead of revealing their haute couture collection. The strategy was simple – make those customers seeking the brands products to do a little extra work to obtain it. The existing content was gone!

Demographics and E-Commerce

Younger generations are dominating the online market and adoption of new technologies. In social media, ages up to 59 account for most accounts, trailing off to just 4.4% of females, and 4% of males over 60. It’s also fair to say that what you’ve grown up with might stick with you through to older age and these stats are likely to change with an older, more digital savvy generation. Might that influence the media sector going forward?

This isn’t the only demographic factor of course. For example, the younger audience tend to prefer video over reading – an interesting fact is that 53% of children in the UK now own a smart phone by age 7, and almost 32% of younger adults pay for video streaming. Such behaviours have already impacted the newspaper world whose expenditure has fallen from £4.45bn in 2005 to £2.8bn in 2020, a decrease of 37% – and newspaper circulation has been declining for several years as preferences switch to digital content.

And all these signals show a growing tendency for consumers to be attached and attracted to their digital content over the content provider themselves. And savvy producers are embellishing content with multiple channels on which to interact with it – for example, key TV shows such as I’m a Celebrity and Love Island have social media and other platforms to engage consumers.

From an e-Commerce perspective, statistics tend to show a growing preference for digital payments over cash. There was an estimated 10% year-over-year increase in the number of digital payments from 2021 to 2022. Some estimates also put the average paid for digital content per user online at $1,766. The shift in the sector has already begun, and its impacts are already being felt by traditional media organisations such as newspapers. But it’s not just the traditional organisations that are feeling the pinch, the cost-of-living crisis and post-pandemic have seen some big streaming platform names lose subscribers in large numbers, despite the promise of exclusive content. Those unwilling to adapt and evolve may be left behind, and those that do, need to move fast to embrace changing behaviours, innovate, and focus on compelling digital content and how to drive revenue in an online market.

Organisational Influences

An interesting bit of research in the newspaper publishing industry suggests that consumers will prioritise digital publications over print, but the same consumers are reluctant to pay for the digital content. If we look at traditional broadcasters, they too have faced tough competition from the new kids on the block with many forced to support their own streaming services and platforms to service a new online market. A couple of small examples, but ones that underlines the challenges to existing media sector traditional business models.

The message again is that media sector organisations have to adapt and respond quickly. They may need to consider killing off legacy parts of their business that can’t compete with digital content, whilst focusing on new platforms and channels that support growth or spread out via multiple channels such as social media platforms to distribute and attract consumers.

Media Sector organisations, like many others, also face challenges of an evolving workforce – from increased working from home post-pandemic blues, and flexible working to high levels of job vacancies. These are real challenges that can be assisted by technology to facilitate mobile, flexible, and remote working.

Trust is also a big factor impacting the sector. In an age where reputations can be made or lost overnight, it will be important for organisations to maintain trust in their brand. This may include developing strategies to manage mis-leading content. Media organisations may also have to look to their own content supply chain to remove manipulation or influence. In short, the sector is having to expend a lot of resources and effort in developing new ways to maintain trust in their brand and protect their digital and consumer assets and data.

The final aspect of organisational influences is Environment, Social and Governance. ESG is becoming an important topic across all organisations. Investment is growing, doubling from 2016 to surpass $50trn by 2025. To re-enforce this, it is likely that governments will increasingly place regulatory obligations on companies to have an ESG strategy and fund. And for media organisations, the consumers view of ESG may play a part in how they consume digital content. 20.6% of 16–64-year-olds make an online purchase influenced by how eco-friendly the organisation they are buying from is. With millennials and Gen-Z estimated to make up 72% of the world’s workforce by 2029, that workforce will be placing greater emphasis on their employers ESG credentials than ever before.

Conclusion

We have barely scratched the surface of many of these topics but the Sector Impact Dial offers a framework to surface the key trends that may impact your strategic priorities. Now is a crucial time to move to an agile and innovative operating model, or potentially be left behind – and Version 1 can help media organisations innovate and embrace change. We believe that organisations within the sector will have to increasingly adapt, adopt, and innovate to stay relevant and retain revenue. They also need to be highly agile, ready to pivot at short notice and adjust to changing market pressures.

It’s exciting times to be in the media sector, who knows exactly what the future will hold, but it’s sure to be a thrilling journey.

Further Reading

This blog is associated with a more in-depth read Media Sector Trends and Challenges 2023 which features much more information on the Sector Impact Dial.

Version 1’s Media Sector Experience

We come with an understanding of the media sector across the UK and Ireland. This includes well-known broadcasters, publishers, and content providers. We are a trusted partner to operate, innovate and transform services across established players, including:

- International Published and Radio Broadcaster

- UK and Irish Newspapers

- European Telecommunications, and,

- National Broadcasters such as

Our collective experience tells us that things are moving quickly across the sector, but that the fundamental priority is still developing and distributing engaging, and increasingly digital content to drive audience growth and data-driven advertising. Talk to us today.

Blog Sources

The following sources of research and information were used for this paper.